As you are no doubt aware, the Chancellor announced a number of major changes in his post election Budget. Probably the biggest bombshell was the major change to the taxation of dividends.

In essence the government has abolished the 10% tax credit on dividends and replaced it with a £5,000 dividend allowance followed by a 7.5% basic rate tax band, 32.5% higher rate tax band and 38.1% additional rate band.

Although George Osborne indicated that the majority of shareholders would be financially better off following these changes, there is the obvious exception of individuals who operate their business through limited companies and have structured their remuneration packages in a way in which the majority of their income is received via dividends.

Currently, due to the 10% dividend tax credit, individuals have had access to an effective tax free dividend up to the higher rate tax threshold. This was a major contributing factor in many businesses deciding to trade as a limited company.

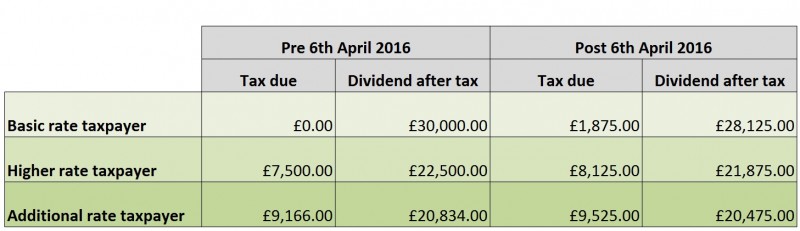

Using a £30,000 dividend payment as an example, the table below gives an illustration of the changes in your dividend tax liability from the current tax year to the tax year beginning 6 April 2016.

With these significant changes in the taxation of dividends many business owners who structured their remuneration to take advantage of the effective “tax free” dividends as a basic rate tax payer will now have a personal tax liability. However, the above table is a simplified one for illustrative purposes and makes a number of assumptions when calculating the tax liability. It is impossible to include the level of detail required on an individual basis and so it is essential that you seek professional advice when deciding upon a remuneration and tax planning strategy for yourself and your business.

There are a wide variety of potential profit extraction strategies available which are dependent on the specific needs of the individuals involved. These include family management buy-out structures (“FAMBO’s”), as well as Employee Shareholder Status type shares which permit shares to be issued with a value of between £2,000 and £50,000 on which tax-free annual dividends of up to £5,000 can be paid, such shares also conferring exemption from Capital Gains tax on sale.

Need help? Want further information?

If you wish to discuss any of the above in more detail or you require assistance with your tax planning strategy please feel free to contact Stephen Elliott on 01942 241103.